Quick Cash from Your Credit Card Here’s What You’re Really Signing Up For

New Delhi [India], June 17: Today, financial flexibility is more valuable than ever. Whether it’s an unexpected medical bill, a last-minute travel plan, or simply a temporary cash crunch, many people turn to a Loan on Credit Card for immediate funds. It’s quick, convenient, and doesn’t involve paperwork. But is it really as simple as [...]

New Delhi [India], June 17: Today, financial flexibility is more valuable than ever. Whether it’s an unexpected medical bill, a last-minute travel plan, or simply a temporary cash crunch, many people turn to a Loan on Credit Card for immediate funds. It’s quick, convenient, and doesn’t involve paperwork. But is it really as simple as it sounds?

While taking a loan on your Credit Card can be a handy short-term solution, it’s important to understand what you’re actually signing up for. From the Credit Card loan interest rate to the repayment structure and hidden charges, there are multiple factors to consider before opting for this form of borrowing.

Let’s take a closer look at how Credit Card loans work, what makes them attractive, and the hidden trade-offs that you should be aware of.

What Is a Loan on Credit Card?

A Loan on Credit Card is an unsecured Personal Loan offered by your Credit Card issuer, typically based on your card usage, repayment history, and credit score. Unlike traditional loans, this is a loan where funds can be disbursed almost instantly, either as a direct transfer to your bank account or as a credit limit lock-in.

Key Features:

- Instant disbursal (in most cases)

- No documentation required for eligible customers

- Flexible tenure ranging up to 60 months

- The loan amount depends on your credit limit or approved limit

Many leading banks and financial institutions, including trusted names like ICICI Bank, offer loans on Credit Cards with a few clicks via Net Banking or mobile apps like the iMobile app.

When Does a Credit Card Loan Make Sense?

There are certain scenarios where a loan on your Credit Card can be a convenient option:

- Emergency expenses (medical, travel, etc.)

- Short-term cash needs without collateral

- Debt consolidation of high-interest loans

- Big-ticket purchases with planned EMIs

Since the loan is unsecured and instant, it’s ideal when you need money quickly and don’t want to go through a lengthy approval process.

How Is It Different from Regular Credit Card Usage?

While it may seem similar, a loan on a Credit Card is structured differently from revolving credit:

| Feature | Credit Card Purchase | Loan on Credit Card |

| Repayment | Pay minimum or full amount | Fixed monthly EMIs |

| Tenure | Usually 45-50 days | Monthly fixed repayment billed on Credit Card |

| Impact on Credit Limit | Reduces available credit | May or may not affect the credit limit |

The Hidden Costs You Need to Know

Before you hit “Apply Now,” t’s important to consider all aspects before proceeding with the application.. Here are the key aspects to examine:

1. Credit Card Loan Interest Rate

The Credit Card loan interest rate is charged as part of your monthly Credit Card bill. If the billed amount, including any EMIs, is not paid by the due date, interest is charged as per the standard Credit Card interest rate. The interest rates start from 13%, depending on the bank, your credit profile, and tenure.

2. Processing Fee

Most issuers charge a processing fee, which may vary by lender. The fees may range from a fixed amount to up to 2% of the loan amount, depending on the loan size and bank policy. Leading banks like the ICICI Bank currently charge a lower processing fee of 1%, making it a more cost-effective option for eligible customers. Always check the fee structure to avoid surprises.

3. Prepayment Charges

Planning to repay the loan early? Some banks may levy a pre-closure fee, typically 2–5% of the outstanding amount. These charges are detailed in the Key Fact Statement and Loan Terms & Conditions. It’s important to review and understand these documents before accepting the loan offer.

4. Reduction in Credit Limit

In many cases, the sanctioned loan amount is blocked against your Credit Card limit, reducing your available credit and potentially affecting your credit score if utilisation remains high.

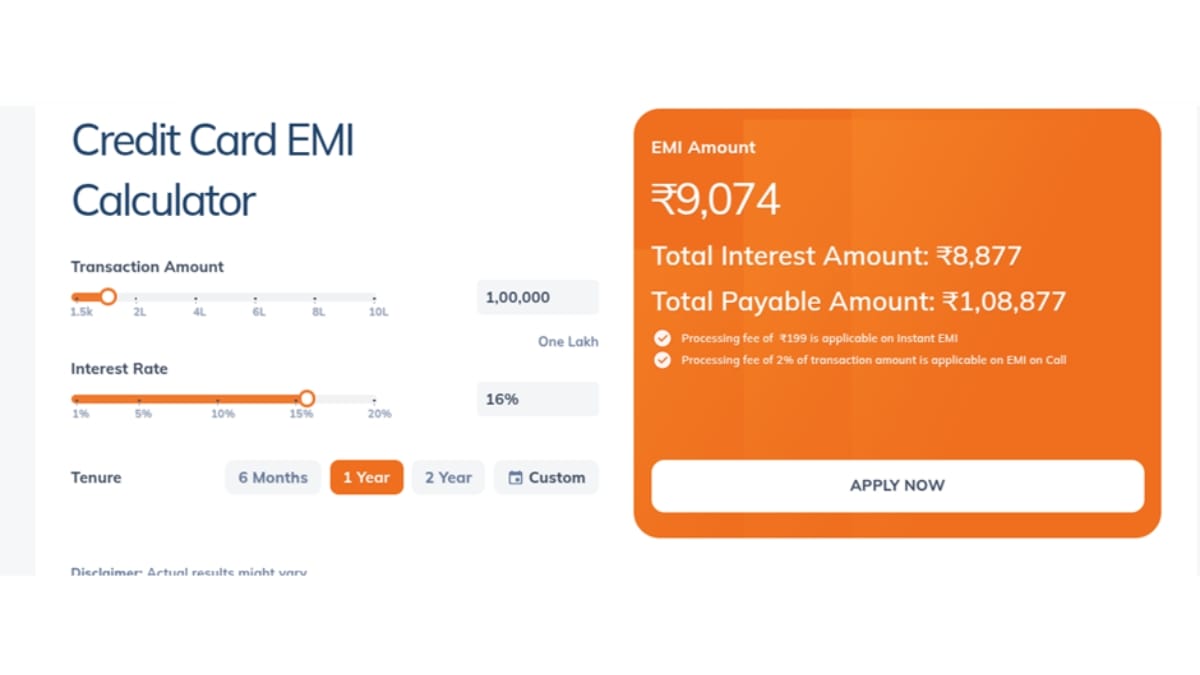

How the EMI Structure Works?

When you take a Loan on Credit Card, you repay it in fixed EMIs, which consist of both principal and interest. These EMIs are billed monthly along with your regular Credit Card bill.

Here’s a quick example:

- Loan amount: ₹1,00,000

- Tenure: 12 months

- Interest rate: 16% p.a.

- EMI: ₹9,074 (approx.)

You end up paying about ₹8,877 in interest over the year. Use online EMI calculators or tools provided by your Credit Card issuer to get accurate figures. These details are also available in the “Key Fact Statement” and Terms & Conditions shared during the digital application process—be sure to review them carefully.

Disclaimer: Actual results might vary

Benefits of Taking a Loan on Credit Card

While there are costs involved, a Credit Card Loan can be a helpful option if used wisely:

Speed and Convenience

No need to submit documents or wait for approval—ideal for emergencies.

Short-Term Funding

Great for short-term cash needs with tenures up to 5 years.

No Collateral Required

These are unsecured loans based on your creditworthiness.

Structured Repayment

Fixed EMIs allow you to budget better than rolling over dues on a regular Credit Card bill.

When Should You Think Twice?

Despite the ease of access, there are situations where this loan may not be the best choice:

- Long-term needs – Interest can add up significantly.

- Existing high Credit Card utilisation

- Multiple existing EMIs – Taking on another one could lead to debt fatigue.

Tips for Using a Credit Card Loan Wisely

1. Use It for Genuine Needs

Avoid taking the loan for discretionary spending or luxury items. Use it only when necessary.

2. Repay on Time

Missing EMI payments can attract penalties and impact your credit score.

3. Track Your Credit Limit

If your credit limit is reduced due to the loan, be cautious about using the remaining balance to avoid overutilisation.

4. Compare Interest Rates

Check if you can get a lower Credit Card loan interest rate from other sources.

Conclusion

A Loan on Credit Card can be a lifesaver during emergencies or when you need quick access to funds. It’s easy to apply, instantly approved in most cases, and repaid via structured EMIs on the Credit Card bill. However, like all credit products, it comes with fine print—interest rates, fees, and credit implications that need to be clearly understood.

If you’re considering this option, make sure you weigh the Credit Card loan interest rate, compare it with other financial products, and use tools like EMI calculators to assess affordability. Many leading banks, including institutions like ICICI Bank, offer transparent loan terms and digital tools to help you make informed decisions.

In the end, a Credit Card loan is neither good nor bad—it’s how and when you use it that makes all the difference.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Investments involve risk, and past performance is not indicative of future results. Readers should conduct their own research or consult with a qualified financial advisor before making any investment decisions.

What's Your Reaction?